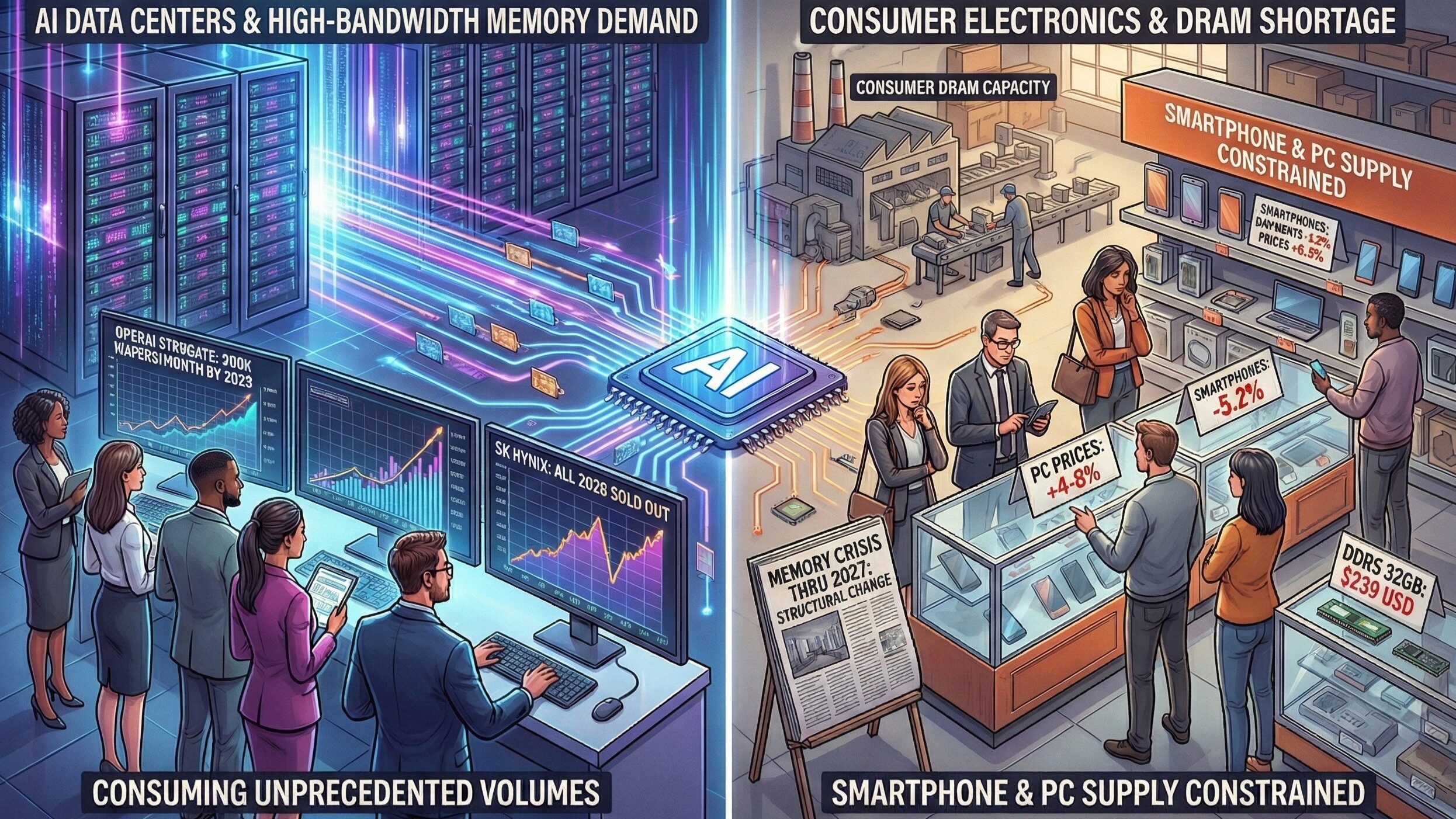

The global memory chip shortage has intensified as AI data centers consume unprecedented volumes of DRAM and high-bandwidth memory. IDC warns the crisis could persist through 2027, with smartphone shipments forecast to contract by up to 5.2% and PC prices surging 4-8% in 2026 as manufacturers prioritize lucrative AI chips over consumer electronics.

What Happened

Memory chip prices have more than doubled since February 2025 as Samsung, SK Hynix, and Micron reallocate capacity from consumer DRAM to high-bandwidth memory for AI accelerators. IDC expects 2026 supply growth at just 16-17% year-on-year, well below demand. OpenAI’s Stargate project alone requires up to 900,000 wafers monthly by 2029, double current global HBM production.

SK Hynix Chairman Chey Tae-won revealed at a Seoul forum the company receives so many supply requests “we’re worried about how we’ll be able to handle all of them.” SK Hynix told analysts the shortage persists through late 2027, with all 2026 production sold out. Inventory collapsed from 13-17 weeks in late 2024 to 2-4 weeks by October 2025. Japanese retailers now limit purchases to eight memory products to prevent hoarding.

Why It Matters

This represents permanent structural change, not cyclical downturn. Three manufacturers controlling 70% of global production deliberately constrain commodity memory because HBM chips generate far higher margins. Micron meets only 55-60% of demand while exiting consumer memory entirely through its Crucial brand closure.

The impact cascades across sectors with immediate consumer price pressure. Smartphone shipments could fall 2.1% in 2026 versus flat-growth forecasts, with average selling prices jumping 6.9% year-on-year. Low-end phones under $200 USD face 20-30% bill of materials cost increases since early 2025. Xiaomi explicitly warns of 20-30% retail price hikes on upcoming models.

PC manufacturers confront similar economics. IDC projects prices rising 4-8% in 2026, with memory now representing 18% of manufacturing costs versus 9% last year. CyberPowerPC cited a 500% RAM cost surge announcing December price increases. Some vendors now ship pre-built systems without RAM, forcing customers to source modules separately in tight markets.

Greyhound Research CEO Sanchit Vir Gogia warned the shortage “graduated from component-level concern to macroeconomic risk” threatening AI productivity gains and hundreds of billions in infrastructure investments. The simultaneous DRAM, HBM, NAND, and hard drive shortage marks what Silicon Motion’s CEO called unprecedented in three decades.

What’s Next

New fabs won’t deliver relief until 2027-2028. SK Hynix committed over $500 billion USD for four facilities, first completing 2027, but allocation between HBM and commodity DRAM remains unspecified. Micron’s Japan plant starts late 2028.

TrendForce predicts continued price increases and spec downgrades through Q1 2026, with low-end phones potentially reverting to 4GB configurations. Gaming PC builders face DDR5 modules at $225-228 USD for 16GB, prompting Epic’s Tim Sweeney to warn of multi-year constraints.

The variable is AI demand. Moderated hyperscaler spending could trigger oversupply by late decade. Sustained growth extends shortages past 2028, reordering semiconductor priorities indefinitely.

Key Facts

- Memory prices doubled since February 2025 in multiple segments with 32GB DDR5 modules jumping from $149 to $239 USD

- IDC forecasts 16% DRAM growth in 2026 versus 35% demand growth, creating persistent supply-demand imbalance

- SK Hynix sold out entire 2026 chip production as of October 2025 announcement

- OpenAI Stargate requires 900,000 wafers monthly by 2029, double current global HBM production capacity

- Samsung raised prices 60% on memory chips between September and November 2025

- Inventory collapsed to 2-4 weeks from 13-17 weeks in late 2024 according to TrendForce

- Smartphone prices may rise 6.9% in 2026 with shipments falling 2.1% per Counterpoint Research

- PC prices expected up 4-8% in 2026 with memory comprising 18% of manufacturing costs

- Micron meeting only 55-60% of core customer demand per December 18 earnings call

- Relief not expected until 2027-2028 when new fabrication facilities complete construction